Racing Accumulator Insurance: How Bookmakers Pay for One Loser in a Five-Fold

The Race You Always Forget

Every accumulator player has the same story. Four legs land, the fifth gets nailed by a 5.0 winner you considered for ten seconds and dismissed. You watch the price you would have collected scroll past in the corner of the screen, and the bet ends with a return of zero. Accumulator insurance is the promotion that addresses exactly that pain – the one-loser scenario that costs accumulator punters more sleep than every other betting outcome combined.

Contents On this page

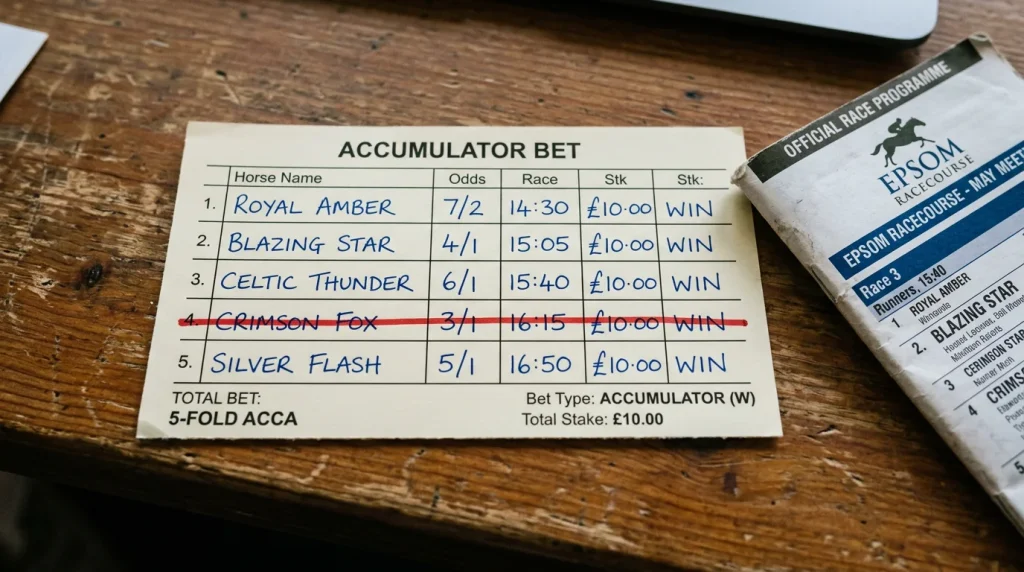

The mechanic is straightforward. Place a four-fold or larger accumulator on UK or Irish racing, and if exactly one leg loses, the bookmaker refunds your stake – sometimes as cash, more often as a free bet. Two losing legs and the promotion does not trigger. Four legs all winning and you collect the accumulator without needing the insurance at all. The promotion exists for the specific middle outcome that accumulator builders fear: the near-miss that returns nothing despite getting most of the bet right.

What makes the promotion work commercially is that one-loser accumulators are actually quite common, and refunds on those bets keep punters building more accumulators. The bookmaker is paying for engagement rather than for an underlying expected-value transfer – the punter who collects an insurance refund typically uses it on another similar bet within days, and the cycle continues. From the operator’s perspective, the cost of insurance is amortised across the much larger volume of accumulator turnover the promotion encourages.

The Conditions That Decide Whether Insurance Pays

Acca insurance does not apply to every multiple. The standard conditions across UK racing operators specify a minimum number of legs – usually four or five – and a minimum price on each leg, typically 1.5 or 2.0. A four-fold of three odds-on favourites and one 6.0 outsider often does not qualify because the cumulative odds or the individual leg prices do not meet the threshold. Bookmakers vary in how they apply these rules, but the underlying logic is consistent: insurance is offered on accumulators that meaningfully add price to the parent bet, not on stacks of short-priced shots.

Maximum refund caps are the second key term. Some operators cap insurance refunds at £10, others at £20 or £25. The cap matters because the insurance value as a percentage of stake declines as you stake more. A £5 acca with a £10 insurance cap is fully covered; a £50 acca with the same £10 cap returns only one-fifth of stake on a one-loser outcome. The promotion is structured to reward casual stakes more than serious ones, which fits the broader pattern of bookmaker promotions in UK racing.

Eligibility on race types varies more than punters expect. Most operators apply acca insurance to all UK and Irish racing; some restrict it to flat racing or to jumps racing; some exclude antepost legs; some exclude legs from particular meetings or tracks. The terms tend to tighten around major festivals – Cheltenham, Royal Ascot, Aintree – because the volume of casual money in the market is highest and the cost of insurance would otherwise spike.

How the Refund Form Changes the Value

Cash refunds are rare on accumulator insurance, despite the way the promotions are often advertised. Most operators issue the refund as a free bet, with all the usual free-bet terms attached – stake not returned, time limit on use, minimum odds on the replacement bet, and frequently a minimum number of legs on any replacement accumulator. The value of a free-bet refund is roughly 65% to 75% of an equivalent cash refund once you account for the typical strike rates and minimum-odds requirements, so a £10 free-bet insurance is worth perhaps £6.50 to £7.50 in expected value terms.

The difference between free-bet refunds and stake-returned refunds matters here exactly as it does for welcome bonuses. The mechanics explained in how stake-returned tokens compare against pure free bets apply identically to insurance refunds – a stake-returned acca insurance is worth materially more than a free-bet acca insurance, even at the same headline cap value. A handful of operators issue insurance refunds as stake-returned tokens; most do not.

The time limit on the refund is the other variable that catches casual punters. A typical acca insurance free bet must be used within 7 days, sometimes 14, with usage often restricted to further accumulator bets meeting the same minimum criteria. A punter who collects a Saturday insurance refund and then takes the next week off racing can discover the refund has expired before they place another qualifying bet. The cost of unused free bets is one of the quiet sources of operator margin on insurance promotions.

Building an Accumulator That Actually Captures the Insurance

The instinct when building an acca for the insurance benefit is to add a deliberately weak leg – the long-priced outsider you would not normally include, on the assumption that if it loses, you collect the refund. This logic is broken for a simple reason: the long-priced outsider is overwhelmingly likely to lose, but it is also the leg most likely to be one of two losers rather than the single losing leg required for the refund. The mathematics of acca insurance reward selections where the single-leg loss is plausible but the double-leg loss is rare.

The shape of an acca that captures real insurance value tends to be four or five legs each priced between roughly 1.7 and 3.5. At those prices, the implied probability of any individual leg losing is between 30% and 50%, the probability of exactly one losing across four legs is in the high 20% to low 30% range, and the probability of two or more losing is significant but not dominant. The total acca price clears typical minimum thresholds, the insurance condition triggers regularly, and the underlying bet has real return potential without insurance.

The pattern I have seen in my own records over the last three seasons is that a 1.8-to-3.5 leg-price range produces insurance triggers on roughly 15% to 20% of qualifying accas, with the underlying bet collecting on roughly 8% to 10%. Add the two and you have a useful return on accumulator turnover when each individual leg is competently selected. Drop the leg prices below 1.7 and the insurance trigger rate falls because the legs almost always win; push them above 3.5 and the trigger rate falls because legs lose in pairs.

The Market Context for Racing Accumulators

The 67.1%/45.1%/35.5% split between football, casino, and racing across the UK gambling participation base masks a more interesting fact about accumulators specifically: racing accumulators are a much smaller share of total racing turnover than football accumulators are of total football turnover. Most racing money is on single horses; most football accumulator money is on multi-leg coupons. That difference has shaped the way operators price their insurance promotions.

Football acca insurance tends to be more generous in absolute cap terms because football accumulators carry higher average stakes. Racing acca insurance tends to be tighter in the maximum cap but more frequent in promotional rotation – operators run racing acca insurance offers more days of the year than football, often as standing weekend offers rather than tied to specific fixtures. The 4.2% turnover decline in UK racing across recent reporting has not changed this – racing acca volume is small enough that the insurance promotions are run as engagement tools rather than as serious cost lines on the operator’s promotional budget.

From the punter’s perspective, the practical implication is that racing acca insurance is reliably available most weekends across the year, including weekday meetings that are not heavily promoted otherwise. A punter who likes to build four-folds on Saturday cards can usually find an insurance offer running somewhere; the question is whether the terms suit the type of accumulator you actually build, not whether any offer is available.

When Insurance Is Worth Including in Your Calculation

The value of acca insurance to your bottom line depends on a calculation many punters skip: comparing the expected return of the insured accumulator against the same selections taken as singles. A four-fold of roughly equivalent prices typically has a lower expected value per pound staked than the same selections as separate singles, before insurance, because the accumulator structure amplifies the bookmaker margin geometrically. Adding insurance recovers some of that lost expected value, but rarely all of it.

The cases where insurance materially closes the gap are those where the insurance refund cap is high relative to the stake – small stakes on accas with generous insurance caps. A £5 four-fold with a £25 insurance cap is structurally different from a £100 four-fold with the same cap. The first is fully covered against the one-loser outcome; the second is only quarter-covered. Casual stakes get more value from insurance promotions than serious stakes, which again fits the wider pattern of how bookmaker promotions are constructed.

The other case where insurance changes the calculation is when the underlying acca is built from selections with positive expected value on their own merits. Insurance on a deliberately speculative acca is largely cosmetic – the underlying bet is unlikely to win and insurance only triggers in a narrow subset of losing outcomes. Insurance on a competently selected acca, where each leg is a bet you would have placed anyway, adds meaningful value because the underlying probability of one-loser-out-of-four is materially higher than the probability of zero-losers.

The Two Promotions That Sometimes Get Confused

Acca insurance is sometimes confused with acca boost promotions, which are structurally different. An acca boost increases the winning return on a successful accumulator by a percentage that scales with the number of legs – a five-fold might get a 10% boost on returns, a six-fold a 15% boost, and so on. The boost only triggers when the accumulator wins; the insurance only triggers when exactly one leg loses. The two are sometimes offered together but rarely stack on the same bet, and the operator terms usually specify whether you choose one or the other.

The other related promotion is acca-builder or request-a-bet markets, where you combine multiple outcomes within a single race or across multiple races into a single priced bet. Insurance promotions do not typically apply to those bets because the structure is not a traditional accumulator – it is a custom market priced as a single bet. Acca boosts also rarely apply to acca-builder bets for the same reason. Punters who use those products need to look for promotions specifically designed for request-a-bet markets, which exist but are less common than traditional acca promotions.

Why Acca Insurance Keeps Pulling Punters Back

Accumulator insurance solves a specific psychological problem more than a specific financial problem. The one-loser accumulator is the bet that gets recounted at the pub for weeks afterwards – the near-miss that haunts punters in a way that an honest two-loser bet does not. The insurance promotion converts that haunting into a tangible refund, and even when the refund is a free bet with reduced effective value, the experience is materially different from a clean loss.

For the disciplined punter, the right way to engage with the promotion is to choose accumulator structures where the underlying selections have merit on their own, where the leg prices fall in the range that produces frequent insurance triggers, and where the cap value is large enough relative to stake to materially cover the one-loser outcome. For everyone else, insurance is a feature that rewards building and rebuilding accumulators on UK racing, week after week, in exactly the way bookmakers want their customers to behave.

How many legs do I need for acca insurance to apply?

Most UK racing operators require a minimum of four legs, with some requiring five. The minimum is published in the offer terms and varies by operator and by individual promotion. Three-fold accumulators almost never qualify for standing insurance offers.

Does it matter which leg loses for the refund to trigger?

No. The insurance triggers on any single losing leg in an otherwise winning accumulator, regardless of which position the losing leg occupies and regardless of its price. The only requirement is that all other legs win and that exactly one leg loses.

Can I get the refund as cash rather than a free bet?

Cash refunds are rare. The standard format is a free bet with the usual terms attached – stake not returned, minimum odds on replacement bets, and a time limit for use. Some operators issue refunds as stake-returned tokens, which carry materially more value, but pure cash refunds on acca insurance have become uncommon.

Articles

Published by the Horse Racing Bet UK team.